2016-Q2 Results released on website

PARADISE GAS CARRIERS CORP

Quarterly Management report

Date : 30/06/2016

Quarterly results (in USD thous.)| BALANCE SHEET (end of period) | 31/12/2015 (audited) | 31/3/2016 (unaudited) |

30/6/2016 (unaudited) |

|||||

| Cash & cash equivalents | 15,543 | 16,181 | 14,441 | |||||

| Other Current Assets | 6,557 | 9,265 | 8,966 | |||||

| Total Current Assets | 22,100 | 25,446 | 23,407 | |||||

| Fixed Assets, net | 66,031 | 64,785 | 63,540 | |||||

| Vessels under construction | 23,775 | 26,801 | 27,286 | |||||

| Deferred drydocking costs | 4,258 | 3,906 | 3,565 | |||||

| Other Non-Current Assets | 2,000 | 2,000 | 2,000 | |||||

| Total Assets | 118,164 | 122,938 | 119,798 | |||||

| Current portion of LT debt | 5,741 | 4,135 | 2,540 | |||||

| Shareholders’ loans | 0 | 0 | 0 | |||||

| Other current liabilities | 5,284 | 4,786 | 2,872 | |||||

| Total Current Liabilities | 11,025 | 8,921 | 5,412 | |||||

| Long-term debt | 29,639 | 28,656 | 29,639 | |||||

| Other non-current liabilities | 1,581 | 1,581 | 1,581 | |||||

| Total Liabilities | 42,245 | 40,141 | 36,632 | |||||

| Paid-in capital | 68,750 | 71,500 | 71,500 | |||||

| Retained Earnings | 7,169 | 11,297 | 11,666 | |||||

| Shareholders Equity (Book NAV) | 75,919 | 82,797 | 83,166 | |||||

| INCOME STATEMENT | 31/12/2015 (audited) |

2016/Q1 (unaudited) |

2016/Q2 (unaudited) |

31/3/2016 (YTD results) |

30/6/2016 (YTD results) |

|||

| Operating Revenue | 40,002 | 11,203 | 9,566 | 11,203 | 20,769 | |||

| Less: Voyage Expenses | (1,190) | (351) | (690) | (351) | (1,041) | |||

| Less: Commissions & Chartering Fees | (580) | (190) | (161) | (190) | (351) | |||

| TCE Earnings (net) | 38,232 | 10,662 | 8,715 | 10,662 | 19,377 | |||

| Operating expenses (excl. man fees) | (16,099) | (3,452) | (3,639) | (3,452) | (7,091) | |||

| Management Fees (related parties) | (1,304) | (328) | (327) | (328) | (655) | |||

| Charter hire expenses | (2,509) | (1,039) | (694) | (1,039) | (1,733) | |||

| G+A Expenses | (301) | (62) | (115) | (62) | (177) | |||

| EBITDA | 18,019 | 5,781 | 3,940 | 5,781 | 9,721 | |||

| Depreciation | (5,313) | (1,246) | (1,246) | (1,246) | (2,492) | |||

| Amortisation | (940) | (360) | (366) | (360) | (726) | |||

| Gain on Vessels’ disposal, net* | 392 | 165 | 165 | 165 | 330 | |||

| EBIT | 12,158 | 4,340 | 2,493 | 4,340 | 6,833 | |||

| Interest Expenses, net | (1,684) | (419) | (377) | (419) | (796) | |||

| Other finance expenses | (501) | (10) | (16) | (10) | (26) | |||

| Extraordinary & other expenses, net | 38 | 58 | (29) | 58 | 29 | |||

| Net Income | 10,011 | 3,969 | 2,071 | 3,969 | 6,040 | |||

| Out of book adj. (codification of borr cost) * | 718 | 138 | 463 | 138 | 601 | |||

| Net Income adjusted | 10,729 | 4,107 | 2,534 | 4,107 | 6,641 | |||

| Dividends distributed | 3,960 | 1,073 | 1,073 | 1,073 | 2,145 | |||

| CASH FLOW STATEMENT (period) | 31/12/2015 (audited) | 2016/Q1 (unaudited) | 2016/Q2 (unaudited) | |||||

| Cash from Operations | 11,151 | 4,598 | 1,403 | |||||

| Cash from Investing | (616) | (2,909) | – | *PGC IKAROS was sold and leased back | ||||

| Cash from Financing | (933) | 1,051 | 3,143 | |||||

| Change of cash in periods | 9,603 | 638 | (1,740) | |||||

| FY15 | 2016q1 | 2016q2 | ||||||

| Loan repayments (net**) | (6,280) | (1,633) | (1,633) | **Net of refinancing proceeds/prepayments | ||||

| STATISTICS (during quarter) | 12m2015 | 2016/Q1 | 2016/Q2 | |||||

| Average # of Ships Owned during Period | 6.0 | 6.0 | 6.0 | incl. chartered-in vessels | ||||

| Average Age of Fleet at end of Period | 13.4 | 13.7 | 13.9 | |||||

| ShipYears Left | 57.5 | 56.0 | 54.5 | Assumed 26 yrs for LPG’s and 20 for Tankers | ||||

| Fleet Valuation ($mill) – end period | 104.1 | 103.0 | 98.5 | FMV: VesselsValue.com(adj as per note 1),incl. NB advances | ||||

| Leverage | 28.0% | 26.3% | 26.4% | Total Dept / (FMV incl. NB advances + Currect Assets) | ||||

| Market NAV ($mill) (1) | 86.0 | 90.4 | 87.2 | See note 1 below | ||||

| Paid-in capital ($mill) | 68.8 | 71.5 | 71.5 | |||||

| Enterprise Value (EV) | 105.80 | 107.95 | 104.98 | EV = Market NAV plus debt less cash | ||||

| Book NAV per 100 usd invested ($) | 110.43 | 115.80 | 116.32 | Book NAV divided by paid-in capital | ||||

| Market NAV per 100 usd invested ($) | 125.04 | 126.37 | 122.01 | Market NAV divided by paid-in capital | ||||

| Dividends received per 100usd invested ($) | 6.0 | 6.0 | 6.0 | 12m cumulative dividends received for 100 usd invested | ||||

| RoE (annualised)* | 15.6% | 20.7% | 12.2% | *Net Income/Total equity (average of last period), includes capital gain | ||||

| RoA (annualised)* | 9.6% | 13.6% | 8.5% | *Net Income/Total Assets (average of last period), includes capital gain | ||||

| EV/EBIT (annualised) * | 8.23 | 7.63 | 7.52 | *EV (today) / EBIT (TTM) | ||||

| P/E* | 8.06 | 7.30 | 6.46 | *Market NAV/Net Earnings (TTM) | ||||

| Dividend Yield * | 4.61% | 4.47% | 4.73% | *Dividends distributed in the last 12m (TTM)/Market NAV | ||||

| Average TCE per Ship, net* | 18,461 | 19,527 | 16,064 | *Net of BB charter hires | ||||

| Average Opex per Ship ($/pd), incl. man fees | 7,947 | 6,923 | 7,264 | incl. management fees | ||||

| Average charter hire expense per Ship ($/pd) | 1,146 | 1,903 | 1,271 | BB charter-in hires | ||||

| Average GA & other costs per Ship ($/pd) | 137 | 114 | 211 | |||||

| Average debt-service per ship ($/pd) | 3,637 | 3,757 | 3,680 | incl. debt-service, other finance costs as well as deferred finance charges | ||||

| Cashflow TCE Breakeven per Ship | 12,866 | 12,697 | 12,426 | includes charter-in costs (approx. $2k/pd) | ||||

| Cashflow Margin | 43.5% | 53.8% | 29.3% | includes charter-in costs | ||||

| Income Statement TCE Breakeven per Ship * | 12,737 | 12,308 | 11,623 | *excl. capital gain | ||||

| Ownership Days (average) | 365.00 | 91.00 | 91.00 | |||||

| Available Days efficiency (2) | 94.6% | 100.0% | 99.4% | See note 2 below | ||||

| Operating Days efficiency (3) | 94.1% | 100.0% | 99.4% | See note 3 below | ||||

(2) Available Days Efficiency is the ratio of the days that the fleet was available for revenue generating; divided to the Ownership days

(3) Operating Days Efficiency is the ratio of the days the ships were actually employed (TC or Spot) and generating revenues (after deducting the off-hire days); divided to the Ownership days

Capital at work

Net Asset Value of $100 Invested in PGC from the start

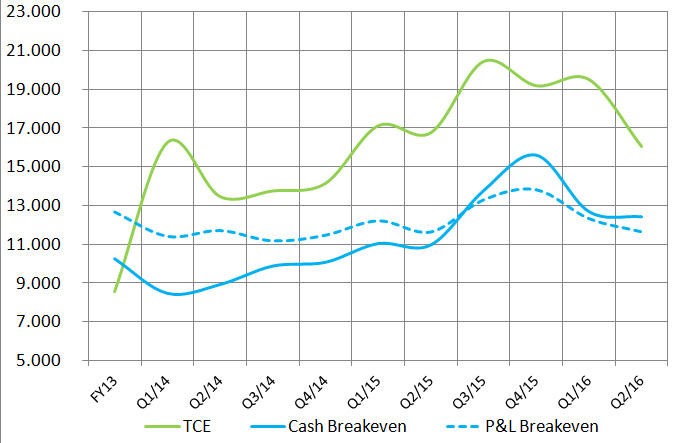

TCE vs cash / p&l b-even

- Management Report & Commentary Q2-2016

- PGC Audited Financial Statements 2015

- Management Report & Commentary Q1-2016

- Management Report & Commentary Q4-2015

- Management Report Q3-2015

- Unaudited 2015-Q3 Financial Statements

- Unaudited 2015-Q2 Financial Statements & Commentary

- Unaudited 2015-Q1 Financial Statements

- PGC Audited Financial Statements 2014

- Unaudited 2014-Q3 Financial Statements

- Management Report Q3-2014

- Unaudited 2014-Q2 Financial Statements

- Management Report & Commentary Q2-2014

- Management Report Q1-2014

- PGC Financial Statements 2013 audited by PWC